Hong Kong’s Diamond Recovery Is About Trade Flows, Not Demand

- May 25

- 4 min read

Hong Kong’s diamond trade grew in the first quarter, signaling an uptick in global flows rather than a meaningful recovery in regional demand across China and the broader Asia Pacific market.

The improvement was evident across both the polished and rough sectors.

Historically, Hong Kong has served primarily as a polished trading center, functioning as a zero-tax gateway for diamonds entering Asia Pacific, particularly Mainland China.

The city also maintains a significant retail jewelry market, and imports have historically exceeded exports, suggesting that part of the polished trade supports demand from domestic jewelers.

However, while Hong Kong serves as the corporate base for leading jewelers such as Chow Tai Fook, Luk Fook and Chow Sang Sang, much of their jewelry manufacturing takes place in Mainland China. Polished diamonds flowing through Hong Kong for manufacturing purposes are typically sent across the border, where the jewelry is produced before being distributed to stores throughout China and back into Hong Kong. These companies also carry out much of their diamond manufacturing in-house.

Where, then, are the primary destinations for the diamonds flowing through Hong Kong?

The Polished Trade

It’s worth noting that Hong Kong is coming off an exceptionally weak period for its polished trade. Imports in 2025 fell to their lowest level since the 2009 global financial crisis, while exports reached their weakest value since the pandemic. As such, growth in 2026 is being measured against a relatively low base.

Polished imports grew 9% year on year to $2.98 billion in the first quarter, while volume increased 1% to 2.98 million carats., according to data published by the Diamond Federation of Hong Kong, China. The average price rose 8% to $999 per carat. Exports increased 7% to $2.71 billion, while volume was flat at 2.71 million carats. The average export price rose 7% to $1,004 per carat.

Growth was largely driven by the major trading centers. Following the post-pandemic surge of 2021 and 2022, imports from India, the US, the United Arab Emirates (UAE) and Belgium have largely stabilized, while shipments from China have declined. The US has notably emerged as a net supplier rather than a net consumer of Hong Kong’s of polished trade.

At the same time, exports to the key consumer markets of the US and China, as well as to Singapore, Thailand and Japan, have weakened, while those to India have rebounded and shipments to Belgium and the UAE have stabilized.

These trends have also been evident at the Hong Kong jewelry trade shows in March and September, which have seen their influence diminish in recent years amid a sharp decline in Chinese buyer attendance.

The data therefore suggests that Hong Kong’s polished trade is currently being supported more by its role as a global trading and logistics hub than by a meaningful rebound in regional jewelry demand.

The increase in flows between major trading centers points to dealers repositioning goods across geographies, while the lack of broad-based export growth into consumer markets reflects the continued caution among retailers and buyers across China and Asia Pacific.

The Rough Trade

The increase in Hong Kong’s rough trading tells a different story, particularly given the current state of the market. That said, India and Belgium also registered an increase in their rough trade during the first quarter.

Hong Kong’s rough imports grew 36% year on year to $311.1 million during the period, with volumes jumping 121% to 3.78 million carats, while the average price declined 28% to $82 per carat.

Similarly, rough exports rose 43% to $338.4 million, with volumes surging 165% to 3.8 million carats and the average price falling 46% to $89 per carat. Alongside the broader decline in rough prices, the data suggests Hong Kong’s trade shifted increasingly toward lower-value goods.

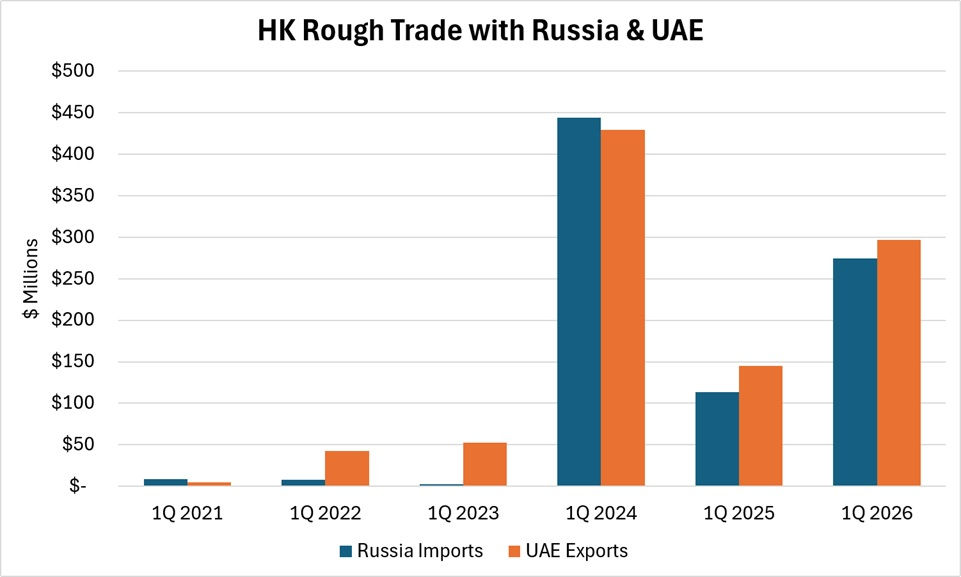

Imports were driven by a 142% surge in supply from Russia to $274.5 million, accounting for 88% of the total. Russia represented 68% of Hong Kong’s rough imports in full-year 2025. Similarly, the UAE remained the dominant export destination for Hong Kong rough, accounting for 88% of exports in the first quarter and 77% for full-year 2025.

The data highlights the city’s role as a transit route for Russian rough into other markets, and particularly to the UAE.

Hong Kong’s imports of rough from Russia and subsequent exports to the UAE have largely moved in tandem over the past five years, with both spiking in 2024, falling in 2025 and rebounding again in 2026.

The increase began in 2024 following the G7 sanctions on Russia-origin rough diamonds. Alrosa, Russia’s dominant producer, historically relied heavily on Belgium as a trading hub, but shifted goods toward alternative centers, particularly the UAE and Hong Kong. Much of that rough is ultimately destined for India for manufacturing, reflecting the continued restructuring of global diamond trading routes following the sanctions.

Shifting Flows

What does all this say about Hong Kong’s role in the diamond market?

Clearly, Hong Kong’s diamond activity has declined significantly from its peak in 2017, when total rough and polished trading – imports plus exports – reached $37.72 billion from 54.3 million carats. By 2025, total trading had fallen to $23.07 billion from 43.6 million carats.

That decline has largely mirrored the slowdown in Chinese demand, which weakened sharply in 2019, deteriorated further during the Covid-19 period, and came under renewed pressure again in 2024 and 2025.

Hong Kong’s improvement in the first quarter, in which total diamond trading increased 11% by value and 51% by volume, should therefore be viewed more in the context of the city’s role as a trading hub within a fragmented global diamond market than as a reflection of jewelry demand in China and Asia Pacific.

The polished trade continues to rely heavily on inter-center trading activity, supported by Hong Kong’s tax-free status, while the rough sector has become more closely tied to the restructuring of supply routes following sanctions on Russian goods.

The first-quarter recovery should therefore be viewed cautiously. The rebound reflects shifting trade flows and inventory movement far more than a broad-based recovery in consumer demand. That said, Hong Kong’s diamond trade may simply have bottomed in 2025.

Graphs: Based on data published by the Diamond Federation of Hong Kong, China.

Image: Registration at the March Hong Kong International Jewellery Show. (Credit: Hong Kong Trade Development Council)

Comments